Both the U.S. and Vermont real estate markets are exhibiting stability and signs of long-term health. While some local markets are seeing slight price corrections due to rising inventory and more balanced supply/demand dynamics, these shifts are part of a necessary and sustainable market normalization.

| Single-Family January-June 2025 | ||||

|---|---|---|---|---|

| Median Sale Price: | Average Sale Price: | Units Sold: | Newly Listed: | Days on Market: |

| $500,000 | 5.3% | $571,265 | 3.1% | 1,005 | 8.9% | 1,723 | 20.1% | 43 | 4.9% |

| Condos January-June 2025 | ||||

|---|---|---|---|---|

| Median Sale Price: | Average Sale Price: | Units Sold: | Newly Listed: | Days on Market: |

| $370,000 | 7.3% | $407,904 | 3.2% | 305 | -10.8% | 494 | -0.2% | 42 | 90.9% |

At the national level, housing experts remain optimistic. According to the latest Home Price Expectations Survey from Fannie Mae, over 100 leading economists and analysts predict that home prices will continue to rise over the next five years, averaging 3.3% annual appreciation through 2029. Even the most conservative projections still forecast annual gains of 1.3%, while optimists expect growth closer to 5%. Crucially, no group surveyed anticipates a decline in national home values, thanks to factors such as low foreclosure rates, stable lending, and near-record levels of homeowner equity.

Mortgage rates remain a headwind for many buyers, but the pressure is easing. The average 30-year fixed mortgage rate now stands at 6.72%, down 17 basis points from this time last year. This modest shift has spurred a meaningful rebound in buyer activity: purchase applications are up 25%. As mortgage rates continue a gradual downward trend, buyer confidence appears to be strengthening across many regions. Most consumers now accept that mortgage rates will not return to the historically low 3.0-4.0% range. Learn more about local mortgage trends from Union Bank.

Inventory is also improving nationally. While some seasonal dips have occurred—particularly around the July 4th holiday—the overall trend is upward. New listings are increasing, and price reductions are becoming more common, a sign that sellers are adjusting expectations in response to rising competition and elevated borrowing costs. At the same time, homeowner equity remains a powerful market stabilizer. More than 82% of U.S. homeowners have at least 30% equity, and the national loan-to-value ratio is at a low 46.9%. In Vermont, over 85% of homeowners are equity rich, meaning they have at least 50% equity in their property; making sellers well positioned for their next move. With the majority of homeowners locked into long-term, fixed-rate loans and experiencing wage growth, there’s little pressure to sell under duress.

What are the latest market trends in Vermont real estate?

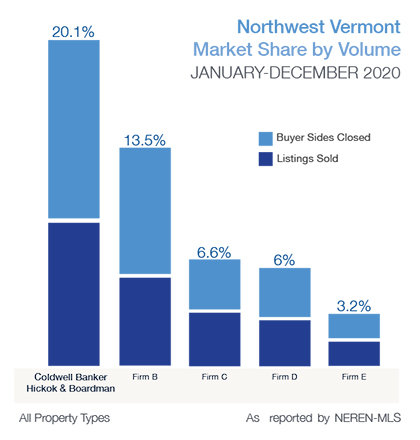

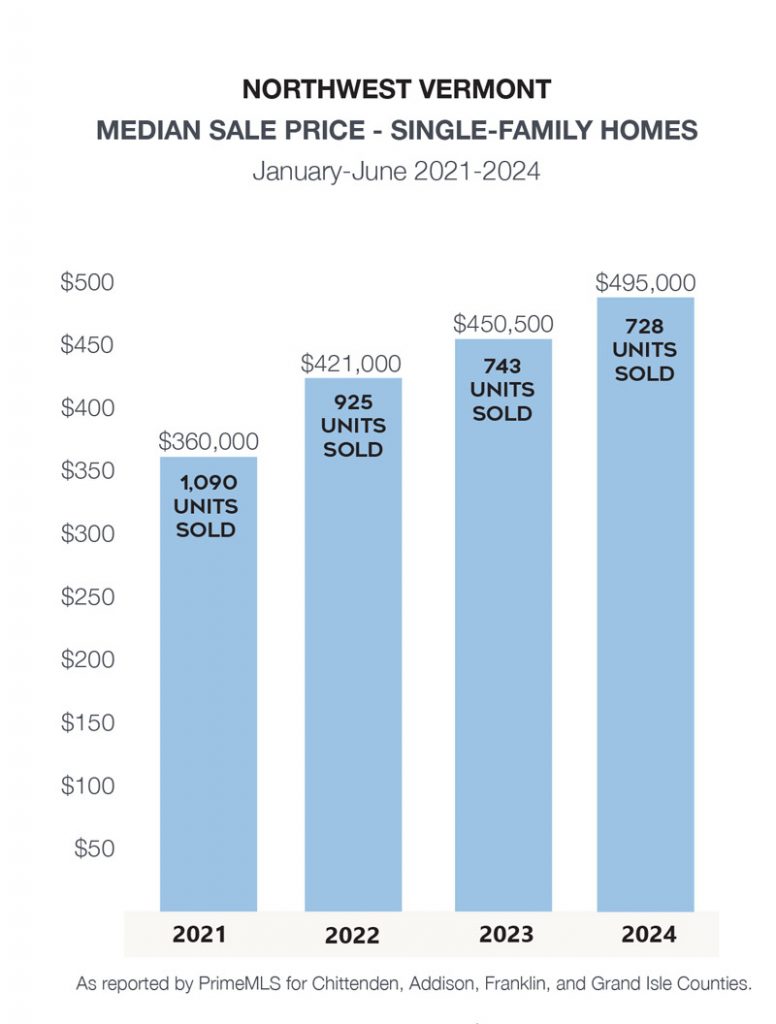

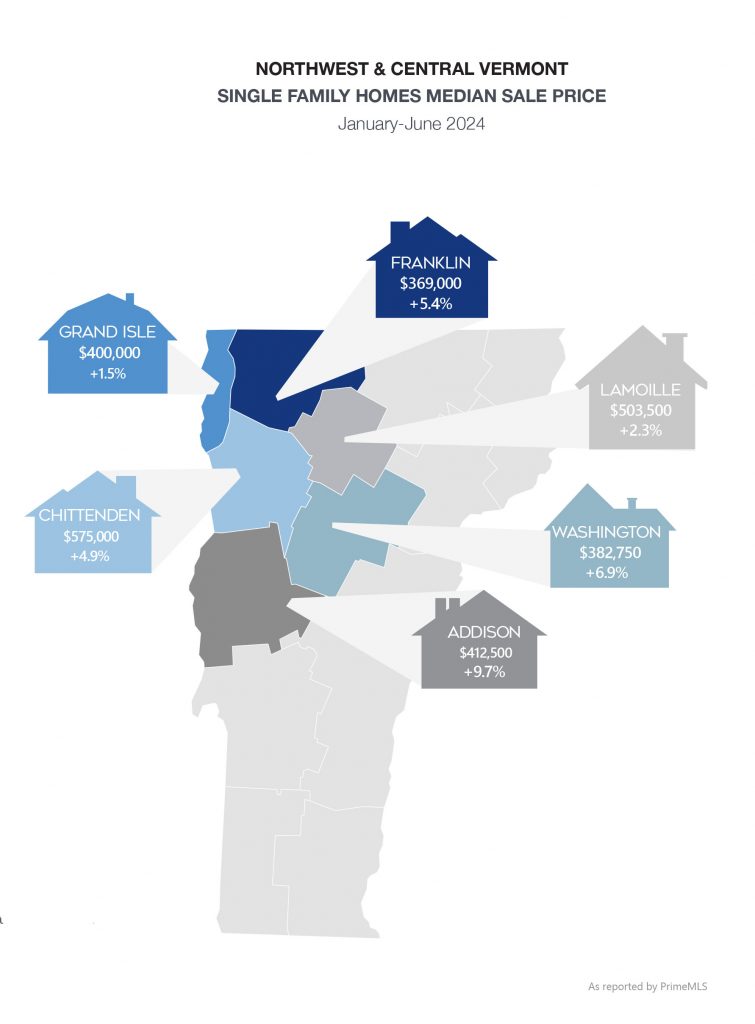

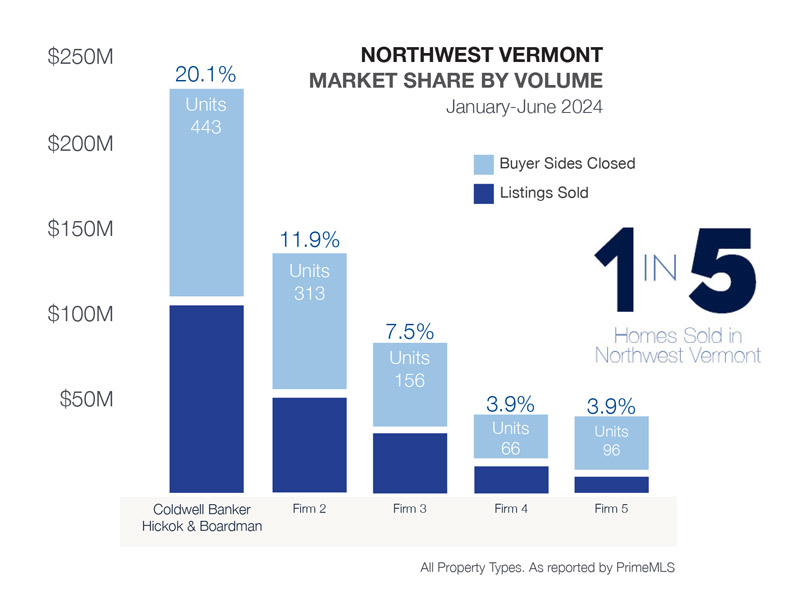

In Vermont, the market reflects many of these national patterns but also exhibits some unique local dynamics. In northwest and central Vermont, the median sale price for single-family homes has climbed to $500,000, a 5.26% increase from last year. This marks a continuation of an eight-year trend that has seen prices rise nearly 89% since 2017. Sales volume is also up, with 1,005 homes sold so far this year—a 9% increase over 2024. Homes are taking slightly longer to sell, with the average days on market rising to 43, indicating a return to more thoughtful, less hurried decision-making among buyers.

The luxury real estate market across the United States and in Vermont is evolving into a more balanced, strategic space where buyers are discerning, sellers must be thoughtful, and opportunities are still available.

Despite global economic uncertainty, the upper tier of the housing market is proving its resilience—fueled by equity gains, wealth preservation strategies, and shifting generational demand.

The multi-family sector is the standout performer in Vermont, with median sale prices up 26.9% and average sale prices up over 33%. Units sold are up nearly 28%, fueled by investor activity and demand for flexible housing options. Condo prices also rose (up 7.25%), though the number of units sold declined, potentially due to supply limitations or shifting affordability. The land segment saw an 8% decline in median sale price, yet sales still rose by 3.57%, highlighting continued interest in development opportunities.

Buyers in Vermont, like their national counterparts, are gaining more time to explore and negotiate. Inventory is expanding, with new listings for single-family homes up 20%, and sellers are responding by pricing more strategically. The high equity environment and steady wage growth among Vermont homeowners offers a strong financial foundation that helps maintain market confidence.

Footnotes:

- PrimeMLS, PrimeMLS.com,

- Fannie Mae, Home Price Expectations Survey (HPES),

It is unclear if there will be a Fed rate cut in 2024 – which many experts were hoping for. If

It is unclear if there will be a Fed rate cut in 2024 – which many experts were hoping for. If

Forecasts from Lawrence Yun, the Chief Economist for National Association of Realtors, suggest a potential 14% increase in home sales this year, accompanied by modest price appreciation estimates ranging between 2.5% to 5%. Despite some buyers anticipating price declines, local market conditions driven by supply-demand imbalances do not support such expectations. Various economists and institutions, including the Mortgage Bankers Association and Fannie Mae, predict mortgage rates hovering around 6% to 6.5%, a level deemed acceptable by both buyers and sellers, capable of stimulating market activity. Additionally, external factors such as the presidential election year, Federal Reserve rate adjustments, and global geopolitical developments could exert further influence on the real estate landscape in 2024.

Forecasts from Lawrence Yun, the Chief Economist for National Association of Realtors, suggest a potential 14% increase in home sales this year, accompanied by modest price appreciation estimates ranging between 2.5% to 5%. Despite some buyers anticipating price declines, local market conditions driven by supply-demand imbalances do not support such expectations. Various economists and institutions, including the Mortgage Bankers Association and Fannie Mae, predict mortgage rates hovering around 6% to 6.5%, a level deemed acceptable by both buyers and sellers, capable of stimulating market activity. Additionally, external factors such as the presidential election year, Federal Reserve rate adjustments, and global geopolitical developments could exert further influence on the real estate landscape in 2024.

The current higher

The current higher

The biggest factor impacting the

The biggest factor impacting the  In 2023, sellers should adjust their expectations. With higher interest rates, there still are buyers out there but not as many as 2021 and early 2022. Sellers will still reap the benefits of strong equity positions in their homes. Offers may come with inspection and financing contingencies. Understanding the current market conditions affecting their home, sellers will benefit from working with an experienced Agent who can guide them to closing with the best terms for them.

In 2023, sellers should adjust their expectations. With higher interest rates, there still are buyers out there but not as many as 2021 and early 2022. Sellers will still reap the benefits of strong equity positions in their homes. Offers may come with inspection and financing contingencies. Understanding the current market conditions affecting their home, sellers will benefit from working with an experienced Agent who can guide them to closing with the best terms for them.

2021, the second year of the pandemic, saw record-setting in sales volume and capped two years of record price appreciation in real estate sales. The impact of the pandemic, coupled with historically low mortgage interest rates in the low 3% range, drove sales up and inventory levels to new record lows to start 2022.

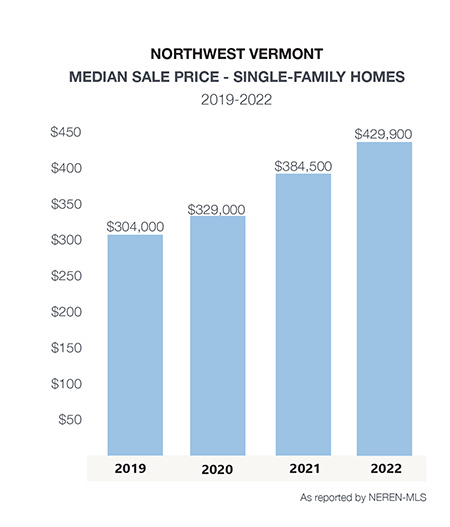

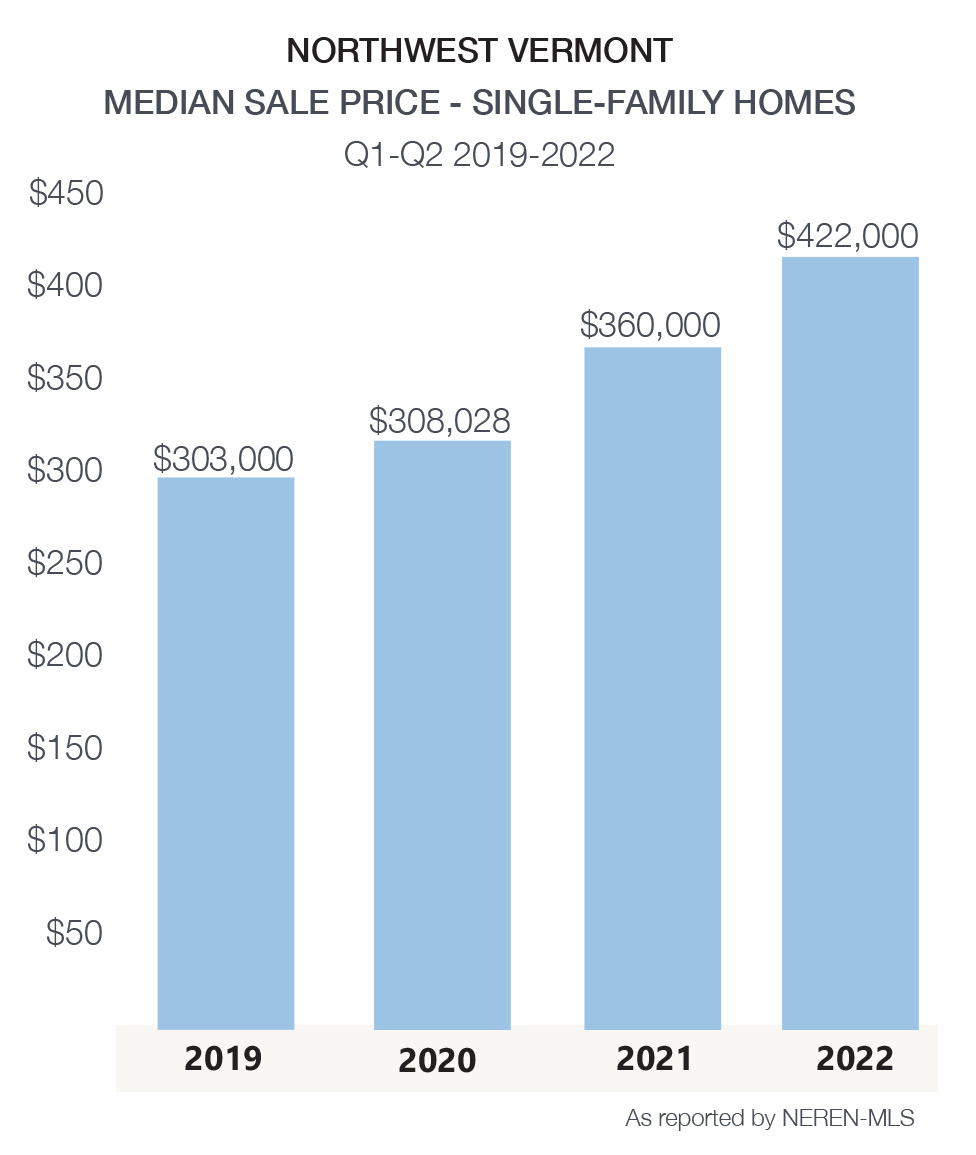

2021, the second year of the pandemic, saw record-setting in sales volume and capped two years of record price appreciation in real estate sales. The impact of the pandemic, coupled with historically low mortgage interest rates in the low 3% range, drove sales up and inventory levels to new record lows to start 2022. Despite these changes, the year-to-date median sale price increase reported nationally hit a new record of $450,000 in June, a 17% gain from last year. Our local market median sale price of single-family homes was a record $422,000, also a 17% increase from 2021. This accelerated rate is not forecasted to continue at the same pace for the second half of 2022.

Despite these changes, the year-to-date median sale price increase reported nationally hit a new record of $450,000 in June, a 17% gain from last year. Our local market median sale price of single-family homes was a record $422,000, also a 17% increase from 2021. This accelerated rate is not forecasted to continue at the same pace for the second half of 2022.

Savvy sellers, following the

Savvy sellers, following the

Association of REALTORS (NAR) recently reported that first time buyers made up 31% of purchases vs. 35% at the same time last year.

Association of REALTORS (NAR) recently reported that first time buyers made up 31% of purchases vs. 35% at the same time last year.

The outlook for 2021 is continued strong demand from both in state and

The outlook for 2021 is continued strong demand from both in state and